High-Yield, Low Stress: How Coaches Are Thinking About Cash in 2026

This isn’t financial advice—it’s a coach’s perspective on applying the same marginal gains mindset we use in training to where we keep our money.

Pun intended with the image - get it, your cash is untrained - it isn't working (and earning you interest). Sorry for the dad joke (kind of).

As we have said before and will say again - NONE OF THIS IS FINANCIAL ADVICE.

This is educational and informational conversations about finances that we have had with coaches before. If you like this stuff you can go to our YouTube playlist where we talk finance with coaches.

Again - NONE OF THIS IS FINANCIAL ADVICE.

Do your OWN Financial Advice and talk with your financial adviser about this stuff and what is right for you. As far as financial advisers you already know who SCN trusts - Northstar Financial whose founder Allen Giese presented inside Fundamentals 1 on financial robustness. They (Northstar and other finical firms) are financial experts and can give financial advice. We, cannot, and are not.

We are talking about the topic with you. If you enjoy this conversation and this topic consider checking out Fundamentals of Entrepreneurship for Strength Coaches from Kosta Telegadas M.S.Ed, B.S., CSCS, XPS. From April 2 - April 15, 2026 you can save $25 on the course with code TAX2026 (case sensitive) at checkout to save. You have until April 15th 2026 at 11:59p to save

With that, here we go with Mike's blog,

Justin

Introduction: The "Marginal Gains" of Banking

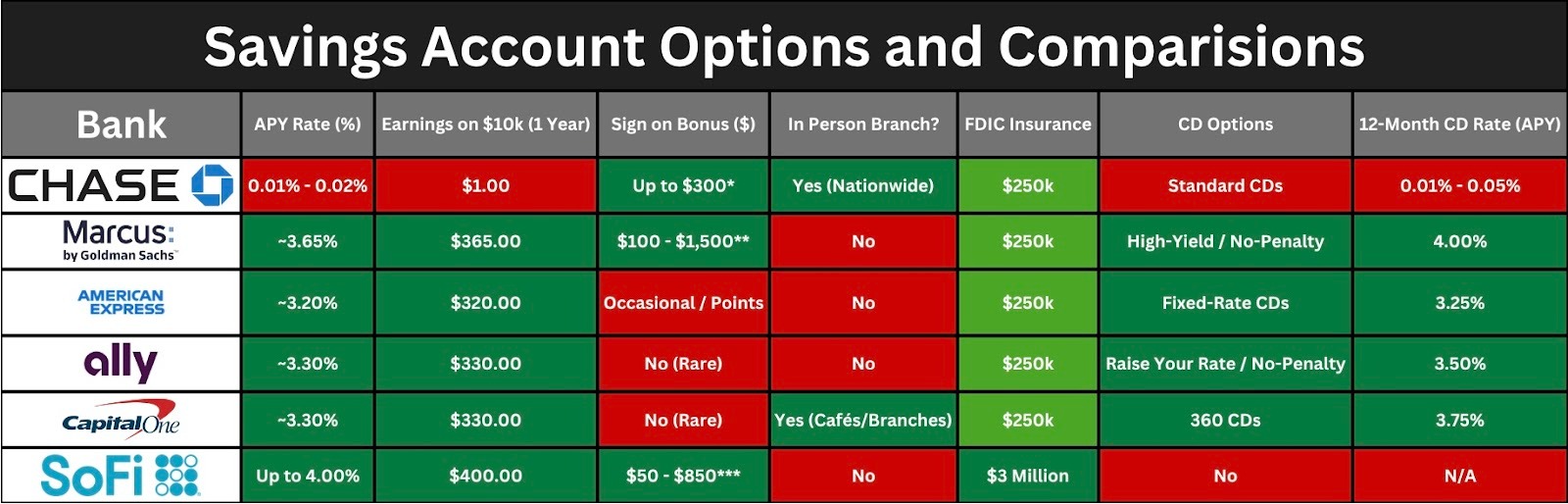

In the world of performance, the marginal gains and percent improvements of speed, strength and power of anywhere between 2-5%+ can ultimately dictate an athlete being under the radar to earning millions of dollars for their contracts. The same can be said for your finances. Leaving your cash in a checking and savings account with big banks such as Chase, Wells Fargo and Bank of America can ultimately lead you to missed opportunities to increase your capital without having to do anything special.These banks (Chase, Wells Fargo and Bank of America) ultimately earn you on average an Annual Percentage Yield (APY) rate of 0.01-0.02% which is TERRIBLE for your financial growth. For example, if you are fortunate enough to have $10,000 in your bank account and you decide to go with Chase earning 0.01% APY, you will only earn $1 for the year. These actions would be no different than training an athlete through a program that fails to utilize the principles of progressively overloading the individual overtime through a training program.

However, if you decided to go with another High Yield Savings option that earns you anywhere from 3.3-4.0% APY, you could potentially earn $330-400 per year on your $10,000. Get the picture?

Just like we all aim to maximize our athletes’ programs, you all should be doing the same with your finances. Even if you feel like you don’t have enough money to start, these options don’t require a minimum deposit to start. So, start small and take action now to evaluate your strategy of what to do with your cash on hand!

Look no further than the Top 5 options for High Yield Savings Accounts for 2026. Spencer Johnson discusses in his YouTube video, the “5 Best High Yield Savings Accounts for 2026” that he published on March 23rd, 2026.

Why should we go for a High Yield Savings Account? Well, they are simple, Federal Deposit Insurance Corporation (FDIC) insured of up to $3 million dollars and the top 5 options in this post are massively competitive compared to the big banks that are failing you. In this post, I will discuss these options he laid out in this video and also provide realistic opportunities for you all to consider with your own financial situations.

The "Top 5" Breakdown (As featured in the video)

I will start the Top 5 Breakdown from the bottom and then work all the way down to the top. These options down below would easily justify taking action today to ditch your big bank savings account entirely and look no further than these options.5. Marcus by Goldman Sachs: Simple HYS that gets it done well.

I currently have this account option and I have had a pleasant experience with this bank. This option in my opinion is the best option for someone that wants a simple HYS account only situation for a great rate.✅ Currently, they are offering 3.65% APY which is one of the best on the market.I personally love this app experience because of their

- Simplicity

- Sleek look and design inside the app.

- There are also no fees for transferring funds

- Transfers in my experience occur within a day period.

However, you could do this.

- Open a Marcus by Goldman Sachs account

- Keep your Chase Checking account open.

- If you have $10,000 or less, you could keep most of the funds within your Marcus account

- Use the Chase Checking account for taking cash out and paying off other bills you have for the month.

4. American Express: Another Simple HYS that gets it done with superb customer service

Currently, they are offering a 3.30% APY rate for their HYS. This is another great option to maximize your savings rates.

American Express is also a well trusted bank institution and strive in these ways

- Customer service

- Reputation

- Simplicity

- Strong Credit Card options

3. Ally

Currently, they are offering a 3.20% APY rate for their HYS. This is another great option to maximize your savings rates.

This bank takes simplicity a step further with offering you different tools to work with within the application.

- Organize your savings into Savings Buckets

- Travel Fund

- Coaching Budget

- CEUS

- Living Expenses

- Set up your Booster to organize your funds into the buckets you want them to go into

- Little to no thinking on your part

- Simple tools that automate the experience and work as a well oiled machine long term

2. Capital One 360 Performance Savings Account

Currently, they are offering a 3.20% APY rate for their HYS. They are FDIC insured of up to $250,000 and there is no direct deposit requirement to continue earning their APY earning rate.

If you value an in person experience, Capital One has In person Cafe’s for in person customer service options. If you have one of their credit cards and have a Capital One Cafe in your area, you get 50% off of coffee as a cardholder when you visit.

Their online app is also a good experience overall from a:

😀 Simplicity Standpoint

🧹 Clean look

🏠 Keeping everything in one place

Speaking of keeping everything in one place, you also have the opportunity of earning 3.75% APY for their 12 month CD if you have available funds to store for a while.

If you are already a Capital One customer and possess some of their credit card options, this can be a good place to keep not only your credit card information, but also your High Yield Savings as well (Capital One, 2026).

1. SoFi Checking/Savings: All in One Option

MASSIVE OPPORTUNITY:

Earn an $850 sign on bonus signing up with Spencer Johnson’s link through Rakuten to open up a SoFi Checking/Savings Account following these steps.

- Click on Spencer Johnson’s link that leads you to opening SoFi account through Rakuten

- Click on SoFi account opening option (Earn a total of $400 through Rakuten + $50 for using Spencer’s link) = $450

- Set up SoFi account

- Accumulate $5,000 from direct deposits in 25 days to receive $400 from SoFi. Anything less than $5,000 from direct deposits in 25 days will be a $50 bonus from SoFi

As of today, the SoFi savings account option currently earns 3.30% APY. Brand new users received an additional 0.7% APY for 6 months. So, for six months, you’ll receive 4.0% APY with this savings account option. In addition to receiving the Savings account, you also get a checking account as well that’ll earn you 0.5% APY.

Coach’s Tip

Note, that you need to set up direct deposit in order to get the entire 3.30-4.00% APY rate. So take the time to set up your direct deposit from your job or side business income.

For those of you that are looking to legitimize your side business, look no further than Kosta Telegadas’ course, Fundamentals of Entrepreneurship. He recommends using Stripe to automate your payments professionally into your banking account. If you have a Stripe account, link up your Stripe account to your SoFi (Telegadas 2025).

Since there are no transaction fees for having money come out of your SoFi account, you would be able to link up your SoFi account to all of your cards and not be charged anything. The strategy here from what Spencer discussed in the video would be to keep most if not all of your funds in your SoFi savings account and link your cards for auto pay withdrawals to your SoFi savings account.

With your Rakuten earnings, you can potentially turn those cash back rewards of $450 into 45,000 Amex or Bilt points if you currently have either an American Express or Bilt card. My personal recommendation from watching Spencer Johnson’s content is that if you have an American Express (such as the AMEX Gold) or Bilt credit card (earn points on rent and mortgage transactions without transaction fee) and travel more than two times a year, then transfer those point earnings to those accounts to stretch your money further for travel redemptions (American Express and Bilt 2026). If you don’t travel often or don’t care enough to get into the weeds of travel redemptions, then don’t sweat the technique (SoFi, 2026).

Spencer Johnson’s HYS Principles for Coaches

🛟 Safety First

Every one of these is FDIC insured from thousands to millions of dollars. All of these options will ensure that your cash remains secure from fraud and discrepancy.

2️⃣ The "Two-Day" Rule

Expect 1-2 days for transfers. Don't put your immediate operating expenses here; keep those in checking. Anticipate that there will be a delay and be prepared for immediate expenses that may arise.

📊 Variable Rates

These rates move with the Fed. For instance, if you are thinking that you have Capital One 360 of 3.20% APY and you want to go to Amex Banking that has 3.30% APY for a slightly better rate, I wouldn’t bother. Don't "rate chase" over 0.10%; pick one and stick with it.

Remember the basic principles. Maximize your cash as much as you can and learn as much as you can from individuals such as Spencer Johnson who create valuable finance content on YouTube. If you have any questions at all, please reach out to me at my email mike@coachmbbrown.comor my instagram @coachmbbrown. Thanks for reading everyone!

Sources

Spencer Johnson YouTube Video Citation

Johnson, S. (2026, March 23). 5 Best high yield savings accounts for 2026 [Video]. YouTube.https://youtu.be/-FvIKgiEVG0?si=9GEgeaH9LQU1NsT9

Kosta Telegadas’ Fundamentals of Entrepreneurship Course

Telegadas, K., & Strength Coach Network. (2025). Fundamentals of entrepreneurship [Online course].https://strengthcoachnetwork.com/Fundamentals_of_Entrepreneurship

Banking & Source Citations

Ally Bank. (2026). Ally Bank rates - Compare our deposit account rates.https://www.ally.com/bank/view-rates/

American Express National Bank. (2026). American Express® high yield savings account.https://www.americanexpress.com/en-us/banking/online-savings/

Bilt Technologies. (2026). Bilt Rewards: Earn rewards on rent and mortgage.https://www.biltrewards.com/

Capital One. (2026). 360 Performance Savings: High-yield online savings account.https://www.capitalone.com/bank/savings-accounts/online-performance-savings-account/

JPMorgan Chase & Co. (2026). What is a high-yield savings account.https://www.chase.com/personal/banking/education/basics/high-yield-savings-account

Goldman Sachs Bank USA. (2026). Online savings options | Marcus by Goldman Sachs®.https://www.marcus.com/us/en/savings

SoFi Bank, N.A. (2026). High yield savings account - Open online, no monthly fees.https://www.sofi.com/banking/high-yield-savings-account/

Mike Brown

Strength Coach Network